More about interest rate hedging

Why should younger participants use protection?

A personal blogging milestone: a person I don’t know (well) answered an online question from someone I don’t know (at all) by referring to something I’ve written. Hooray!

It was a reference to this post about interest rate risk of young pension participants:

That post ended with a lot of questions, which I want to address in this post:

My starting point is the Merton model, that the balance sheet of younger savers is dominated by the fixed-income asset of their human capital, and participating in a pension fund is a way to transform part of that human capital into risky financial capital. How would their balance sheet benefit from investing instead in fixed-income financial capital? Maybe it has a higher interest rate than human capital? It may be because financial capital is tradeable and contributes a return through rebalancing that human capital doesn’t. Or it may be because the specific features of the WTP allow taking more leverage when investing in fixed-income, rather than risky, financial assets.

On reflection and discussion I believe the main driver of the perceived benefit is the last one: offering younger participants a protection return1 to “hedge” their future pensions provides them with leverage in the WTP system. They gain additional exposure to the term premium without having to reduce exposure to the equity risk premium. And since the term premium is positive and quite low-risk—certainly when considered at the margin of a big equity-risk exposure—it is plausible that adding a bit of this exposure will add value for younger cohorts.

But really this conclusion is an artifact of the framing of the question. Let’s apply that finance superpower: understanding the balance sheet (Wiki):

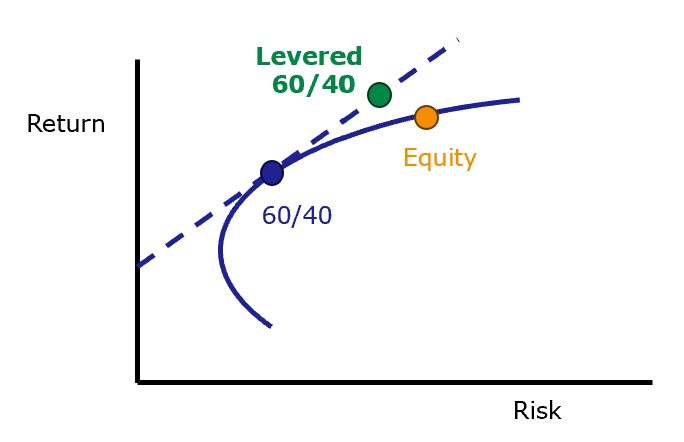

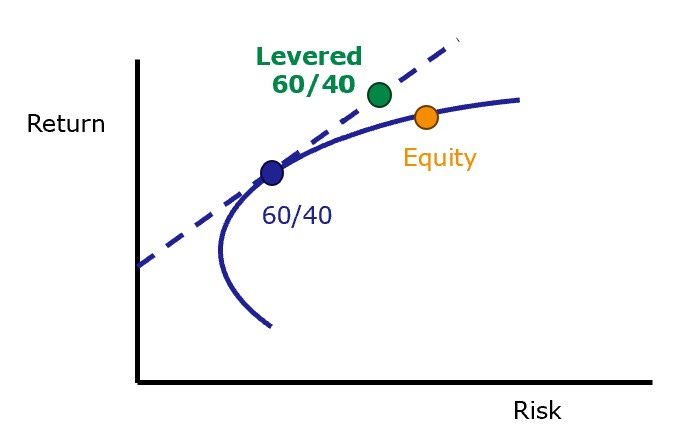

Firstly this reasoning confuses the “overrendement” (excess return, OR) on the right-hand side (liability or owner equity)2 of a funds balance with an equity investment on the left-hand side (asset). A risk-optimal portfolio—on the left of the balance sheet—contains some bonds for diversification and rebalancing from equities (60/40 anyone?) and so provides participants with rates exposure through OR.

Secondly (and relatedly) it muddles the treatment of leverage. If you have identified OR with equities, adding an unfunded rates exposure (i.e. buying bonds with borrowed cash) will, through diversification and rebalancing, improve the risk-return characteristics of the portfolio while increasing leverage (taking your equity portfolio to 100% equities/66% bonds/-66% cash: the 5/3-times-levered 60/40 portfolio!) In my best PowerPoint™ representation of MPT, green beats orange:

To repeat, this figure lives in the asset side of a fund’s balance sheet.

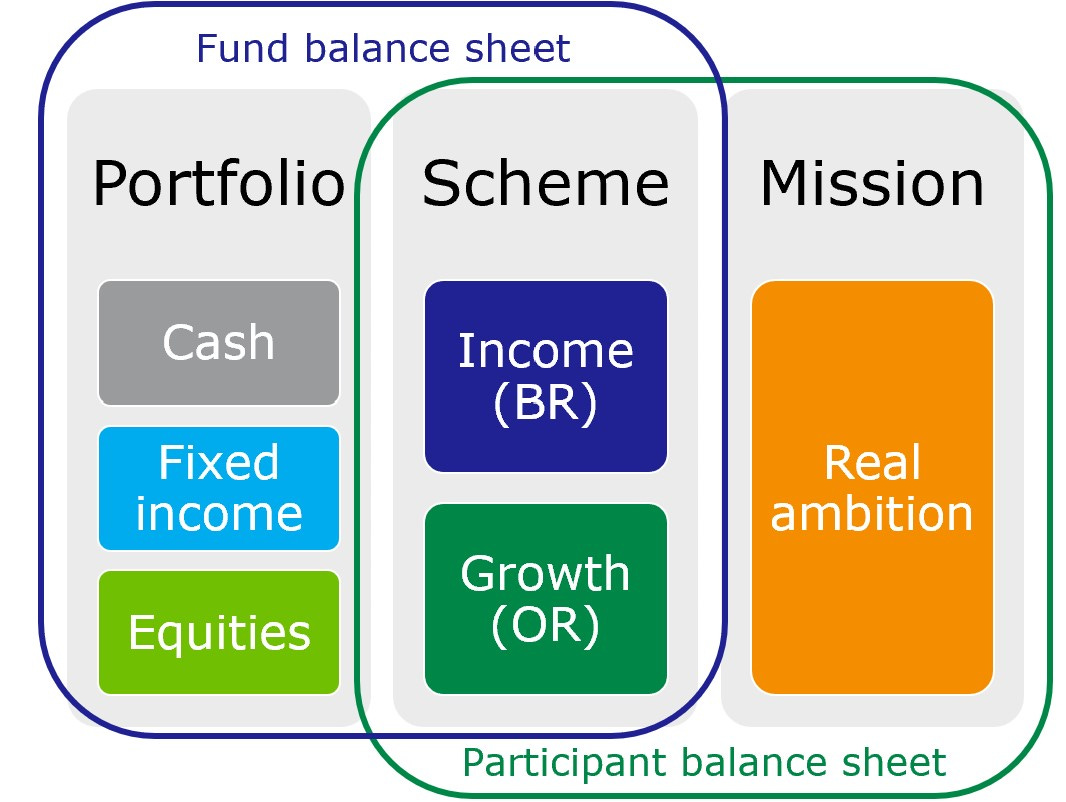

Summarizing, we should not confuse scheme design with portfolio construction. We need our mental model to distinguish at least:

Member ambitions as inflation-protected cashflows;

Two classes of fund liabilities: BR nominal annuities3 (DB) and OR growth returns (DC);

At least three classes of investible assets: equities, bonds4 and cash.

The scheme design takes us from 1 to 2—determining the composition of the participants’ asset holdings—and portfolio construction from 2 to 3—the fund asset allocation given that liability structure. Again channeling my inner PowerPoint™ artist:

The original confusion arises because the OR/DC/growth fund in line 2 is not given, it is created by the pension fund. If you identify it with a vanilla equity portfolio (orange dot) in line 3, member outcomes in 1 are improved by adding rates exposure in line 2. This is not clearly true if the OR-class is created as a levered 60/40 portfolio (green dot), that already captures portfolio benefits of interest rate exposure.

After going on far too long on the topic I think I can finally point to what bothers me about it. That is the circularity of the design: the designing the scheme simultaneously defines and constrains members’ assets and fund liabilities. Without giving participants a say in the scheme here—either the nature of the fund’s liabilities nor the life-cycle allocation to them—we are leaving them with no agency at all over the risk they bear. We could be doing ALM in reverse: design a liability structure suited to the pre-existing investment portfolio and reverse-engineer participant preferences so that they fit that structure. No wonder this technocratic tendency tends to run afoul of the supervisor.

Even with the best intentions of the designers, I believe ultimately individual members know best what’s good for them, even if that includes making the decision what amount of interest rate hedging they find suitable. Of course the vast majority will choose the default option, and those that don’t might choose poorly more often than not. But still, principle!

This post ends the same as did the last one:

Other suggestions welcome, to be (inevitably) continued.

Reference

I chortle thinking of the cover image, but the debate is about pension scheme design.

In writing this post I realized that, annoyingly, there is no English-language equivalent of what in Dutch are called passiva—all entries on the right-hand side of the balance sheet, encompassing both liabilities (vreemd vermogen) and owner’s equity (eigen vermogen). Translating the linked Wiki-page for passiva takes you to the Wiki-page for liabilities.

On the flip side (ha!) activa correspond to assets.

Ideally the annuities would be inflation-linked as well to represent risk-free pensions. Then participants’ risk appetite could be directly implemented as the allocation to their “risky” option, the “owners equity” of the fund. This gets us to the target income paradigm.

Another common simplification is to identify bonds with the nominal annuities.